Taking profits for STI ETF & doubling my stocks purchase to close to SGD$70k in Tiger Brokers

When people talked about STI being the Super Terrible Index, I laughed. It was such an apt description cause the people around me who invested into STI via DCA years back are still seeing red.

Despite that, I decided to take it up when it was hovering around $2.50+ in Sept 2020 through Tiger Brokers. I reckoned that Singapore economy would one day rebound. When would that "one day" happen? I'm not sure. But I figured if it continues that way for the next 1-2 years, I'll just accept the dividends that comes along, since interest rates from saving accounts SUCKS.

I didn't expect STI to cross $3.00 4 months later.

I had also planned to sell it off once it hits $3.00.

Not sure if it was a sign - I came across this, and I quote "A gain is not a real again unless its a realized gain". So I decided to sell off my shares in STI ETF, for a ~18% profit.

All through Tiger Brokers.

You can check out the fee comparison on stocks purchases between Tiger and DBS vickers (cash upfront) in my link here.

Sales commission and fees charges

For my STI ETF sales, I only incurred a commission and GST fee at $3.89 for a sale of 1000 shares. If I had used DBS vickers, I would have to pay a minimum $25 sales charge.

Update on Tiger Brokers portfolio

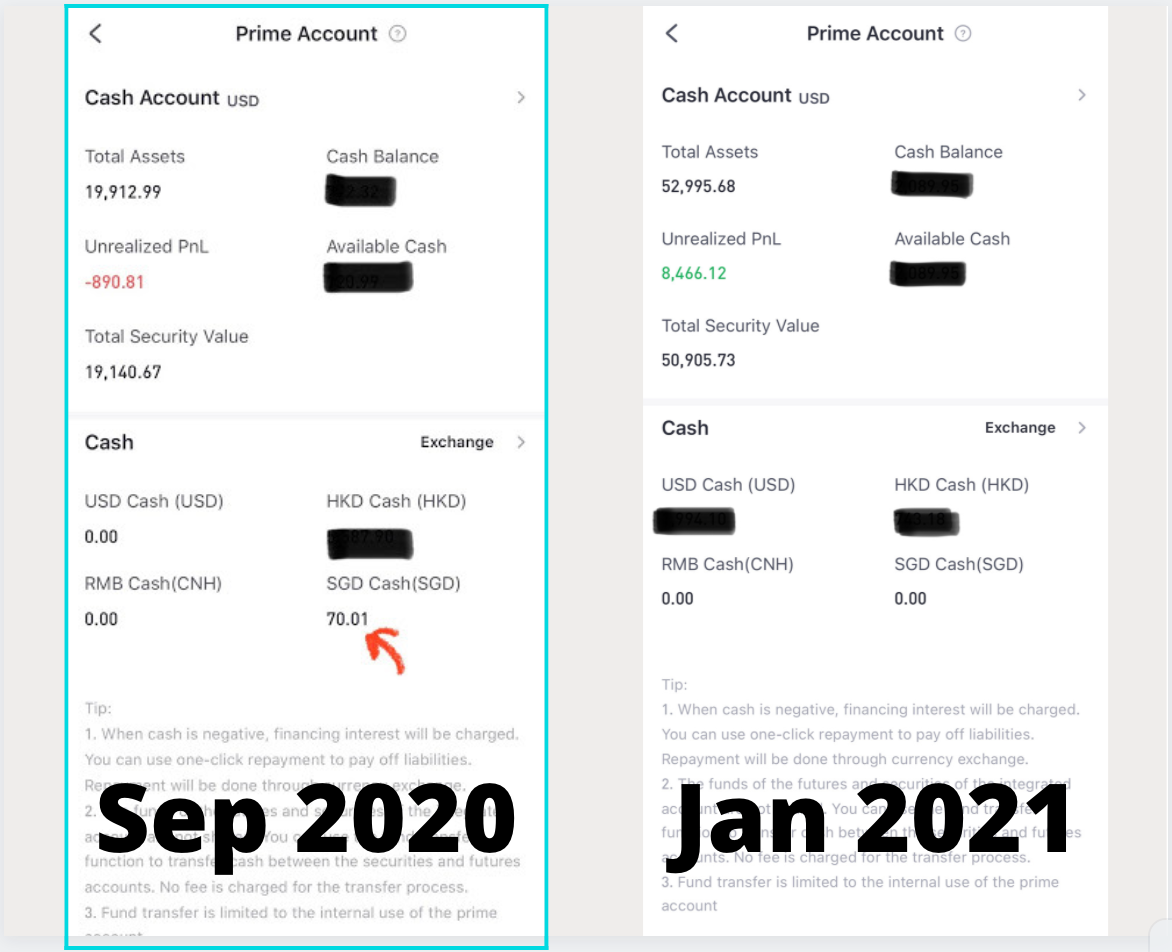

Speaking of my earlier post, I blogged about pumping SGD$28k into HK and Singapore markets in Sept 2020. In 4 months, I've grown it close to SGD$70k and sitting on ~$12k paper gains. Here's a side by side comparison (take note amount in screenshot is in USD):

Meanwhile, I will look at other stocks to channel my STI index profits.

Otherwise, this would serve as a good angbao for myself to buy something I want.

Referral (shameless plug)

If you are keen to use Tiger Brokers and you'd like to receive stock vouchers to offset your stocks purchases, kindly use my referral link, code (SBSL8) or scan the QR code to sign up😊 You can refer to my beginner guide here.

Comments

Post a Comment

No rude messages please. Unkind messages and spams will be blocked and deleted.