6 tips on how I save money when dining out + promo/referral codes

Owning a personal finance blog doesn't mean I scrimp and live a sad life. It also doesn't mean I'm stingy and deprive myself from material stuffs! There are things that I'll never regret spending on....and that is

With no interest in makeup, expensive clothings and bags, these have saved me money... but I do spend quite a lot on food, more so with a gluttony partner. Also, being a boring person, I naturally have nothing interesting to do with my partner except to hunt for good food lah.

I love my hawker food, but sometimes, we gotta spice things up a little when we paktor right? And we all know dining in Singapore is a costly affair.

While I've spent quite a bomb dining out, I've been making use of a few tips for the past few years which helped me save money without killing the joy!

So here are some tips you could use to save money when dining out. You may thank me later :P

1.

I came across the eatigo app two years ago and have been using it ever since. This app not only allows reservations, the most attractive part comes from it's generous discounts! Depending on the time slots you choose, some restaurants offer 50% discount off their menus! I've lost count of the times I've dine at restaurants paying only 50% of the usual price and gleeing away when I pay the bills. And best of all, this app is FREE!

If you're a first time user to eatigo, get $5 rewards for your 1st attended reservation with Eatigo when you download the app from my link or sign up with my referral code 'cherryeat'!

Bonus tip! By reserving your slots through shopback, you'd get to receive $2 cashback! Btw, if you have yet to sign up for shopback, click on my link to get your $10 bonus :)

OMG, this type of lobang where to find?!?!?!?

2.

The Entertainer app has been my most used app this year. The Entertainer offers 1 for 1 vouchers for selected restaurants such as Fat Cow and Bedrock Bar & Grill. If you are looking for a wider variety of restaurants (including fine dining), the Entertainer App is a great addition to the eatigo app above.

Take note that the app is a yearly subscription i.e it offers vouchers for use from 2 Jan 2018 to 31 Dec 2018, so if you wish to make use of the app in 2019, you will need to purchase again.

Personally, one of the main reasons for buying this app was the substantial savings I could clock. For example, around Vday this year, my partner brought me to Bedrock Bar & Grill for their steaks. Without the app, a ribeye for myself would cost him $99++. With the entertainer app, we paid $99++ for the both of us with the 1 for 1 voucher! Considering this, we already saved $99 hor? HAHA. Sometimes my bf grumbles that we spent way more because of the app....I mean, to utilise the app that we've already paid for, we'll go out and source for places to dine at, while we could actually settle for hawker food. Oops!

One difference between this app and eatigo is that this is a paid app. The Entertainer app is free to download and offers you a few basic vouchers to utilise/test it out, however, in order to unlock more deals, you'd need to purchase the app.

Currently, they are having an early bird discount of $95 for 2018 edition which comes with the Cheers app (for the alcoholic...I have not utilised any vouchers in 2017 lol) and Bali 2018 for your use in Bali! I've already bought my 2018 app!

Bonus tip! If you feel that $95 is very chor (expensive) on your pockets, why not share the app with 2 other friends since each restaurant offers 3 vouchers to use?

Just a note - in the past, the app was available for use EVERY DAY. Now, some restaurants stop you from using it on weekends or public holidays. So, do check with the restaurants on the conditions before using it!

3.

If you are new to the fuzzie app, get your free $5 credit to offset your voucher purchase - enjoy cashback on voucher purchases for eg. ezbuy, grab, lazada, klook when you sign up using my link here.

4.

Before fave was Groupon, which was quite a craze some year back where consumers purchase discounted deals. I haven't been using fave much but occasionally when I spot discounted cakes, buffets and vouchers, I'd buy them.

fave frequently runs promotions so keep a look out for their discount codes which could make your deals even cheaper! If you've not downloaded fave yet, enter my promo code W6HZA for a $3 discount or click here to be directed.

Bonus tip! By reserving your slots through shopback, you'd get to receive up to 4.5% cashback! Btw, if you have yet to sign up for shopback, click on my link to get your $10 bonus :)

If you do not have this card, consider using the DBS Visa Debit card which gives you 5% rebate with every paywave transaction!

If you know of a better dining cashback card, let me know in the comments below!

[UPDATED in Dec 2018]

6.

GOOD FOOD

With no interest in makeup, expensive clothings and bags, these have saved me money... but I do spend quite a lot on food, more so with a gluttony partner. Also, being a boring person, I naturally have nothing interesting to do with my partner except to hunt for good food lah.

I love my hawker food, but sometimes, we gotta spice things up a little when we paktor right? And we all know dining in Singapore is a costly affair.

While I've spent quite a bomb dining out, I've been making use of a few tips for the past few years which helped me save money without killing the joy!

So here are some tips you could use to save money when dining out. You may thank me later :P

1.

I came across the eatigo app two years ago and have been using it ever since. This app not only allows reservations, the most attractive part comes from it's generous discounts! Depending on the time slots you choose, some restaurants offer 50% discount off their menus! I've lost count of the times I've dine at restaurants paying only 50% of the usual price and gleeing away when I pay the bills. And best of all, this app is FREE!

If you're a first time user to eatigo, get $5 rewards for your 1st attended reservation with Eatigo when you download the app from my link or sign up with my referral code 'cherryeat'!

Bonus tip! By reserving your slots through shopback, you'd get to receive $2 cashback! Btw, if you have yet to sign up for shopback, click on my link to get your $10 bonus :)

OMG, this type of lobang where to find?!?!?!?

2.

The Entertainer app has been my most used app this year. The Entertainer offers 1 for 1 vouchers for selected restaurants such as Fat Cow and Bedrock Bar & Grill. If you are looking for a wider variety of restaurants (including fine dining), the Entertainer App is a great addition to the eatigo app above.Take note that the app is a yearly subscription i.e it offers vouchers for use from 2 Jan 2018 to 31 Dec 2018, so if you wish to make use of the app in 2019, you will need to purchase again.

Personally, one of the main reasons for buying this app was the substantial savings I could clock. For example, around Vday this year, my partner brought me to Bedrock Bar & Grill for their steaks. Without the app, a ribeye for myself would cost him $99++. With the entertainer app, we paid $99++ for the both of us with the 1 for 1 voucher! Considering this, we already saved $99 hor? HAHA. Sometimes my bf grumbles that we spent way more because of the app....I mean, to utilise the app that we've already paid for, we'll go out and source for places to dine at, while we could actually settle for hawker food. Oops!

One difference between this app and eatigo is that this is a paid app. The Entertainer app is free to download and offers you a few basic vouchers to utilise/test it out, however, in order to unlock more deals, you'd need to purchase the app.

Currently, they are having an early bird discount of $95 for 2018 edition which comes with the Cheers app (for the alcoholic...I have not utilised any vouchers in 2017 lol) and Bali 2018 for your use in Bali! I've already bought my 2018 app!

Bonus tip! If you feel that $95 is very chor (expensive) on your pockets, why not share the app with 2 other friends since each restaurant offers 3 vouchers to use?

Just a note - in the past, the app was available for use EVERY DAY. Now, some restaurants stop you from using it on weekends or public holidays. So, do check with the restaurants on the conditions before using it!

3.

I've previously blogged about fuzzie here where I shared my purchase of the klook vouchers. Fuzzie is a cashback app where you receive cashbacks in the form of fuzzie credits when you purchase gift cards from them. I've previously earned $4 cashback on the $50 klook gift card I purchased.

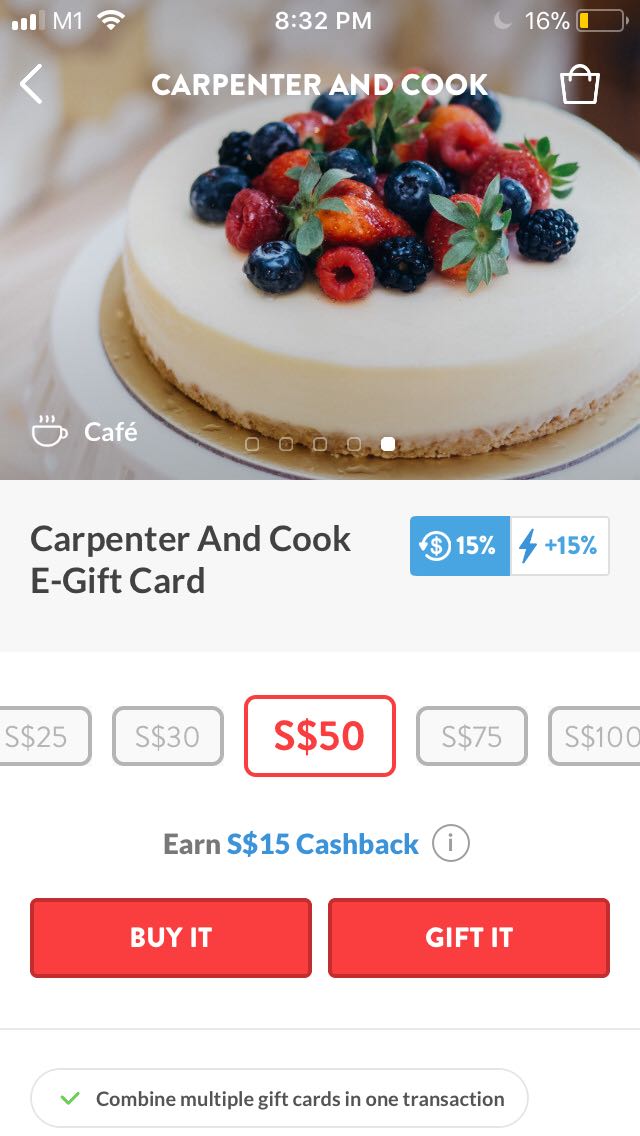

Other than travelling deals, fuzzie offers cashback on food! For example, if you wish to dine at Carpenter and Cook, you could purchase their $50 gift card which earns you $15 cashback....which you could then use to offset other gift card purchases!

The best time to purchase via the fuzzie app would be when they run their power up promotion where you receive extra cashback during this period. However, take note that the gift cards have expiry dates so make sure you read their T&Cs.

4.

Before fave was Groupon, which was quite a craze some year back where consumers purchase discounted deals. I haven't been using fave much but occasionally when I spot discounted cakes, buffets and vouchers, I'd buy them.

fave frequently runs promotions so keep a look out for their discount codes which could make your deals even cheaper! If you've not downloaded fave yet, enter my promo code W6HZA for a $3 discount or click here to be directed.

Bonus tip! By reserving your slots through shopback, you'd get to receive up to 4.5% cashback! Btw, if you have yet to sign up for shopback, click on my link to get your $10 bonus :)

5. Make use of your cards!

When dining out, I'll always use my BOC Family Card to pay the bills. The BOC Family card offers 7% dining rebates everyday. Some cards I know only offers attractive rebates on selected days. Also, BOC offers up to $100 rebates, which means a maximum of $1,428 spend on food a month. I don't spent that much on food la, but knowing that each dining transactions clocks me 7% feels shiok....hahah! But take note of the minimum $500 spendings per month to be eligible for the 7% rebate!If you do not have this card, consider using the DBS Visa Debit card which gives you 5% rebate with every paywave transaction!

If you know of a better dining cashback card, let me know in the comments below!

[UPDATED in Dec 2018]

6.

Ever since I discovered Chope, my partner and I have been using it as a fuss free way to make reservations at restaurants - no more waiting for the restaurants to pick up my calls! Not only is it more convenient for me to book a seat at popular restaurants, with every reservation, I could earn 100 chope dollars!

And the first 400 chope dollars allow me to redeem for a $10 voucher to offset my bill at a wide list of restaurants such as 49 seats, Standing Sushi Bar, Yum Cha and more.

If you are new to Chope, sign up with this link to get 300 Chope dollars on your first reservation!

The good thing doesn't end here. Other than using it to make reservations, we have also been purchasing Chope vouchers to dine at a steal 😆such as a $20 valued-meal at Tim Ho Wan for only $10! My partner and I had a good tea break during our off day heehee

Comments

Post a Comment

No rude messages please. Unkind messages and spams will be blocked and deleted.